‘I’m a civil servant with a £1m pension – should I retire now before Labour’s tax raid?’

Write to Pensions Doctor with your pension problem: pensionsdoctor@telegraph.co.uk. Columns are published weekly. Becky O’Connor is away.

Dear Charlene,

I need some urgent advice, as I suspect many readers do. I am a senior public official (yes, some of us do actually read the Telegraph).

I am lucky enough to be a member of a public sector pension scheme and was looking forward to retirement soon. I am 59 and the main element of my scheme pays out at 60, although I could go earlier with an actuarial reduction.

I intended to take the maximum lump sum as my wife and I wish to invest this in a property abroad – this has always been our dream.

As far as I can make out the value of my pension pot today is around £1.045m but by the end of the financial year it will be something like £1.11m.

All good – except I am now concerned about what changes a new government might make. Not only a reimposition of the lifetime allowance but also potential changes to the tax-free lump sum.

What should/can I do to protect my position? I am prepared to hit the “retire immediately” option though I would need to give three months’ notice.

But would that protect me?

It isn’t a preferred option as I would like to carry on in my current role but I would do it if it was the only way to protect my lump sum plans.

I would be most grateful for any advice you can offer.

Many thanks,

RJ

Dear RJ,

Your main scheme is due to start paying out from your next birthday and your dream holiday home is within touching distance, so it’s understandable that you want to protect your plans.

I’ll explain the pension rules, but it might be worth consulting an international tax expert too, just to make sure you understand the tax implications (home and abroad) of your dream purchase.

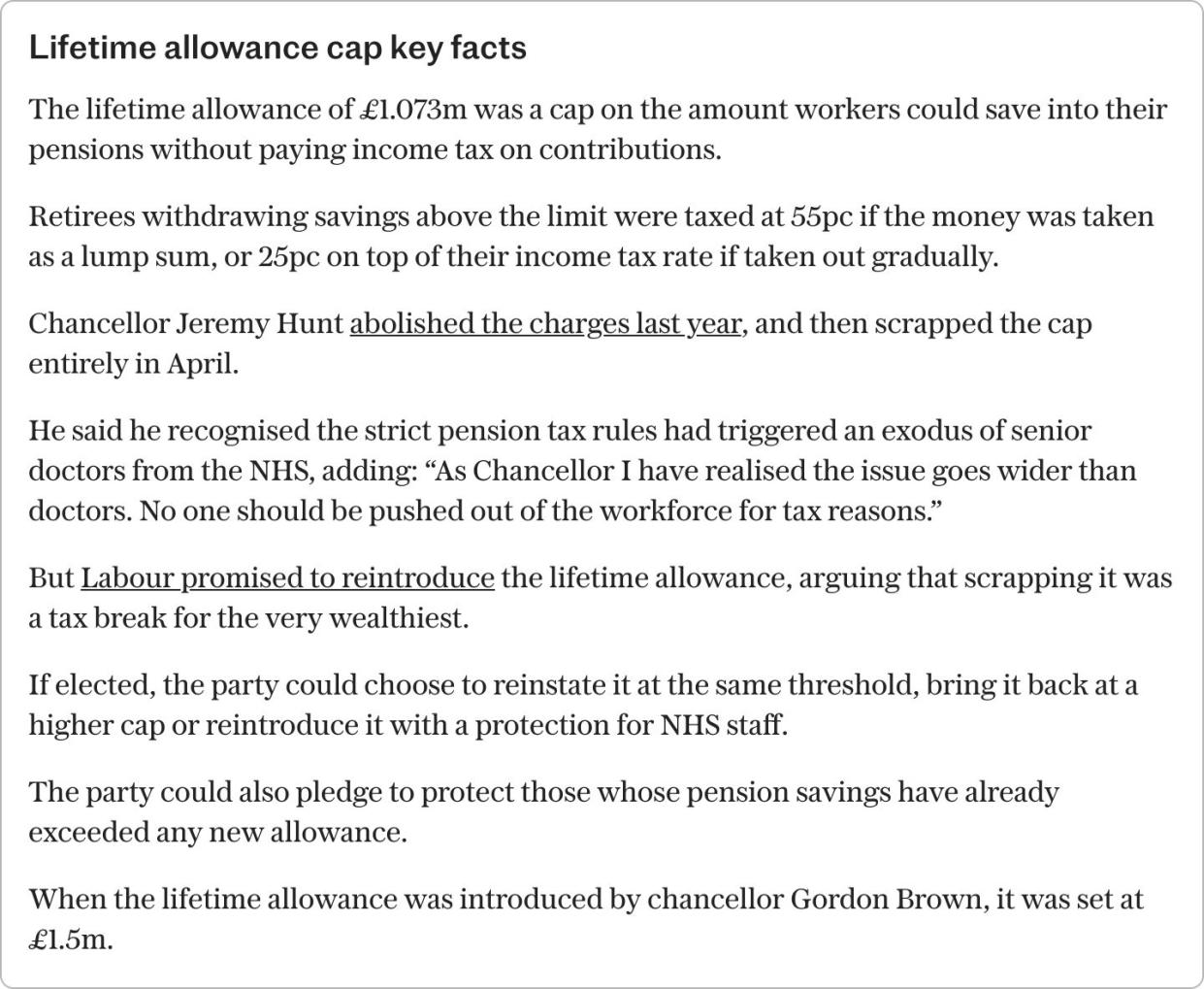

Let’s start with the good news – it looks like Labour has dropped its plans to bring back the lifetime allowance. I’m hoping this gives some comfort to you, as well as anyone else reading this who had their own retirement planning worries.

However, it’s important to be aware that there are several new allowances which have replaced the old lifetime allowance and these may impact your plans.

We’ve now got a cap on tax-free lump sums you can get when you start to draw your pension(s) – this “lump sum allowance” is set at £268,275 (25pc of the old lifetime allowance). There’s also the “lump sum and death benefit allowance” which measures all tax-free lumps paid to you and your beneficiaries. That is set at £1,073,100.

Any excess lump sum is subject to income tax, in the same way as pension income.

Most people can still take up to 25pc of the value of their pension tax-free, and for private pensions like Sipps, it’s easy to work out a quarter of the value of your pot and compare that to the allowance.

For public sector pensions, taking the maximum lump sum will usually mean a reduction in your final pension. Exactly how much depends on your scheme. Based on the numbers in your letter, it’s likely that your maximum lump sum at 60 will be below the lump sum allowance, but not far off. Your benefit statement and online portal can tell you your scheme type, maximum available lump sum and how it’s calculated.

As an example:

Let’s assume a full final pension of £55,000. Assuming an exchange rate or pension-to-lump sum of 1:12 (known as a commutation factor), a £236,000 lump sum would reduce the starting pension to around £35,000 per year.

The lump sum would be lower than the current lump sum allowance, and mean a total pension value of around £1m, under the old lifetime allowance.

Why Labour changed its plans

As well as recognising the uncertainty it would’ve caused pension savers both now and in the future, there is perhaps an understanding of the scale of the task itself. The legislation to remove the lifetime allowance took two years to implement and ran to over 100 pages of technical changes.

And even now, HMRC are having to issue further guidelines and amendments to sweep up anomalies and unintended outcomes, all hallmarks of a rushed job the first time around.

Should you act now?

If you hit the “retire immediately” button, not only do you have to give notice, but you’ll face a reduction in your pension to pay it out early, which is usually around 5pc for every year of early retirement.

This will likely affect your maximum lump sum, and you’d finish work earlier than planned – all factors that need to be weighed up against locking in your position now before we’ve even seen a manifesto.

We haven’t seen the manifesto yet, but indications are that further caps to tax-free lump sums are not part of Labour’s plans. If reintroducing the lifetime allowance was to be a retrograde step, meddling with tax-free cash would surely be the nuclear option.

Your goal to take your maximum lump at retirement would probably mean you sneak under the current tax-free allowance and the time required to sort changes in the law would also mean it’s unlikely to catch you personally anyway.

If you do decide to stay on and retire after your 60th birthday, it’s worth bearing in mind that your pension scheme will need time to do your final calculations and pay out your lump sum and pension. This takes a lot longer than for personal pensions – perhaps even 3 to 5 months – so it’s worth you checking the process with your scheme.

Your personal timeframes are in months rather than years, but the lifetime allowance speculation is a good reminder that, as a general rule, it’s better to try and focus on long-term retirement goals rather than trying to second guess what might happen to the tax system in the future.