How much worse can it get for gold?

Gold hit five-year lows on Monday.

Just when you thought it couldn't get much worse, it has.

Today we consider the two big events of the past week and we ask: "What next?"

Annihilation in New York, shenanigans in Shanghai

In the early hours of Monday morning, with Europe sleeping, America still on its weekend and Japan on holiday, somebody sold 22 tonnes of gold.

To put that number in some context, that's just under 1% of annual global production.

They didn't sell it in Shanghai, or Hong Kong, or Australia, where the markets were busy. They sold it in New York on the COMEX. It was 9:29am in Perth, 2:29am in London, and still Sunday – 9:29pm – in New York.

Markets at this time on Sunday evening are described as 'thinly traded', because nobody's at work.

Yet somebody decided to sell almost 1% of all the gold the entire world produces in a year. They sold it in just four seconds.

There was an immediate reaction in Shanghai and a further five tonnes were sold.

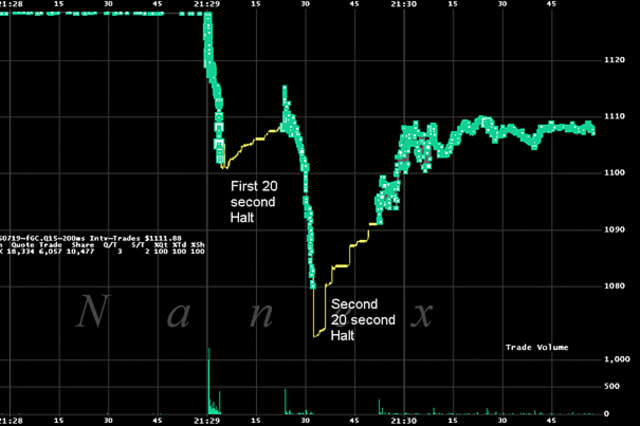

The first wave of selling took the price from $1,130 per ounce to $1,100. Then trading was halted for 20 seconds. There was a slight rebound, then another wave of selling took the price down to $1,070. It all happened in little more than 30 seconds. (My thanks go to Perth Mint's Bron Suchecki for his dissection of all this.)

Here, courtesy of Nick Laird of Sharelynx, is a screenshot of the action.

It's worth noting that the maintenance margin (the amount of money you'd have to have sitting in an account to back your holdings) on these contracts would have been somewhere around $30m.

Over the course of the night, some 57 tonnes were sold in Shanghai and New York, reports Ambrose Evans-Pritchard in The Telegraph, driving the gold price to a five-year low.

On Monday the price recovered a little back about $1,100. But the miners fell by around 10% in a single day. Barrick, the world's largest producer, fell 15%, and Newmont fell 12%.

For three weeks out of the last four, gold has been hit hard in Sunday night/Monday morning trading.

While the Greek panic was on, gold opened higher, only for it to be walloped. This time, gold got whacked when it was already down.

Laird has plotted the minute-by-minute action for each of the past four weeks in the chart below.

The right hand side of the chart shows the Sunday sell-offs, the left the Monday morning follow-through.

As often seems to be way, the price in the paper markets took a hit, just as demand for physical was on the increase. There is a disconnect.

At first glance it seems someone with deep pockets wants the price down. It might be a government or central bank conspiracy, as some suggest. It might (as I find more probable) be speculative funds of some kind shorting gold – trying to get stops hit when markets are quiet.

It might, simply, be the consequence of margin calls in China – its plummeting stockmarket forcing the sale of all assets, much as we experienced in 2008.

The big kahuna that turned out to be a damp squib

This action followed the big news out of China last week – the announcement of China's official reserves, which John wrote about on Monday.

These were last announced in 2009 – 1,054 tonnes – making it the world's seventh largest gold owner. Last week China declared 1,658 tonnes.

Top gold holdings at March 2015

Top gold holdings at March 2015

Rank | Country/Organisation | Gold holdings (tonnes) | Gold's share of forex reserves |

|---|---|---|---|

1 | United States | 8,133.5 | 74% |

2 | Germany | 3,383.4 | 68% |

3 | International Monetary Fund | 2,814.0 | N/A |

4 | Italy | 2,451.8 | 67% |

5 | France | 2,435.4 | 65% |

6 | China | 1,658.4 | 1% |

7 | Russia | 1,275.2 | 13.3% |

8 | Switzerland | 1,040.0 | 7% |

9 | Japan | 765.2 | 2% |

10 | Netherlands | 612.5 | 57% |

Source: Wikipedia/World Gold Council

Since 2009, Laird's data shows China has produced more than 2,300 tonnes – averaging over 400 tonnes a year in (mostly) state-owned mines – to become the world's largest producer. It has imported 3,414 tonnes from Hong Kong. And just under 9,000 tonnes (of which the Hong Kong gold makes up about a third) of physical gold have been withdrawn from the Shanghai Gold Exchange (SGE).

In other words, over 10,000 tonnes of gold have made their way to China.

And it has barely exported an ounce. Its government has even actively encouraged its citizens to own gold, and demand now stands at well in excess of 1,000 tonnes a year (that number may fall this year after the losses on the stockmarket). Annual global production, to put that all in context, is 2,600 tonnes.

The hope among gold aficionados was that China's next announcement about its gold would be considerably larger than the 1,658 tonnes it announced last week. If it had announced 2,500 tonnes, that would have made it the world's third-largest holder after the US and Germany. A (what seemed) entirely possibly 3,400 tonnes would have put it ahead of Germany in second.

Some were even hoping that the number would come in above America's 8,133 tonnes. Naive though that may seem, given the numbers above, it is not beyond all possibility.

But China's gold – at 1,658 tonnes – accounts for little more than 1.5% of its foreign exchange reserves; America's counts for 74%, and Germany's 68%. Even if China's gold were to account for just 5% of its reserves, with over 5,000 tonnes, it would be sending a very strong message to the world – not just that China is rich, that it means business and that it's a challenge to US economic might.

But, more importantly for gold bugs, that message would suddenly legitimise gold as a strategic, monetary asset – the very thing they crave.

The power of such a message on the gold price would have been breathtaking. But the message never came. The disappointment is considerable.

Of course, it's highly possible, if not probable, that China has more gold than it says it does. It might not be declaring all the gold held by all state departments. It might be that it wants to downplay its holdings in order to drive the price down so it can accumulate more on the cheap. It might not yet be ready to throw down such gauntlets to the US.

Or it might be that China is telling the truth and official holdings are as reported.

It doesn't matter. It's made its announcement and probably won't make another for another five years. The trump card that was going to turn this bear market around has been played, that particular narrative is another that has gone the way of the pear, and it leaves even less for gold bugs to cling on to.

The bear market goes on. Gold needs another story to reverse it.

Here comes $1,050 an ounce

My long-stated prediction is for gold to hit $1,050, and it now looks like we're going to see that. If we get there, the next question to ask will be, "Will it hold?" If it doesn't, $850 comes back into play. But there is a lot of support at $1,050. It was a wall of resistance for several years on the way up. Hopefully, it will prove to be support now.

On the positive side, sentiment is overwhelmingly bearish. June to August is the worst period for gold – and usually when you see the lows for the year. Physical buying is still robust. The Indian wedding season (when the most physical buying occurs) is not far away. And the low price is going to put yet more mines out of business, which should shrink production.

Perhaps it's time for a contrarian bet.

More on AOL Money:

Gold pocket watch set to fetch a record £10 million

Roman gold coin reaches £400,000 at auction

Why you should include gold in your pension